》View SMM Silicon Product Prices

》Subscribe to View SMM Metal Spot Historical Price Trends

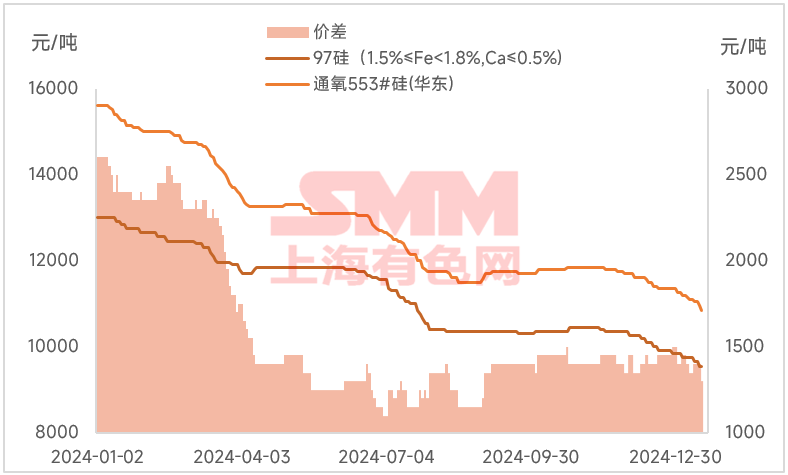

As the Chinese New Year approached, the usual peak season for downstream stocking in previous years did not materialize. The 97 silicon market cooled before the holiday, with both demand and prices weakening. Currently, the ex-factory price of mainstream 97 silicon specifications (1.5%≤Fe<1.8%, Ca≤0.5%) has dropped to around 9,500 yuan/mt. Many 97 silicon manufacturers reported that the current price has fallen below the profit margin, operating below the cost line.

As some 97 silicon manufacturers entered a loss-making phase and downstream procurement demand remained sluggish before the holiday, some manufacturers began taking advantage of the weak market to conduct furnace maintenance. Several manufacturers have scheduled maintenance this month, while a few have cut production capacity for 97 silicon and shifted to other product segments.

Based on current market feedback, the total production of 97 silicon in January is expected to be around 34,000 mt, down approximately 3,000 mt compared to December's total production of around 37,000 mt. Moreover, manufacturers' sentiment remains predominantly pessimistic, with little willingness to resume or restore 97 silicon production in the short term. The production of 97 silicon is expected to continue its downward trend in February.

The recent decline in 97 silicon is mainly due to the suppressive impact of the silicon metal market. With silicon metal prices continuing to fall, the low-price advantage of 97 silicon as a substitute has diminished, and the price spread between 97 silicon and silicon metal has continued to narrow. This has further shifted the already weak downstream end-user demand this year toward silicon metal. Currently, apart from a few large manufacturers maintaining a normal pricing and sales approach, most small manufacturers are unwilling to sign orders at a loss as prices have entered a loss-making stage. They continue to quote at relatively high levels, but new order signings remain scarce. Overall, the market has cooled before the Chinese New Year, with general transaction activity being relatively moderate.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)